Description

What our Financial Literacy: Borrowing vs. Saving to Buy Something lesson plan includes

Lesson Objectives and Overview: Financial Literacy: Borrowing vs. Saving to Buy Something teaches students about saving versus borrowing money to purchase the things they want. At the end of the lesson, students will be able to explain the difference between saving money and borrowing money for an item they want to purchase. They will also be able to weigh options, prices and have a basic understanding of comparative shopping and will understand that credit adds cost to purchases. This lesson is for students in 5th grade and 6th grade.

Classroom Procedure

Every lesson plan provides you with a classroom procedure page that outlines a step-by-step guide to follow. You do not have to follow the guide exactly. The guide helps you organize the lesson and details when to hand out worksheets. It also lists information in the blue box that you might find useful. You will find the lesson objectives, state standards, and number of class sessions the lesson should take to complete in this area. In addition, it describes the supplies you will need as well as what and how you need to prepare beforehand. The supplies that you will need for this lesson include pencils, pens, and highlighters.

Options for Lesson

Included with this lesson is an “Options for Lesson” section that lists a number of suggestions for activities to add to the lesson or substitutions for the ones already in the lesson. One optional addition to this lesson is to have a loan officer from a bank come in to speak with your students about credit scores and interest rates. The lender can also bring examples of loans for things like cars, homes, or other ordinary everyday items and loans that were not approved, which your students can analyze and explain why some loans are approved whereas others are not. Then, assign a group of students to be lenders and others to be borrowers. Next, have students fill out a loan application for a house, car, or other items. Then, pretending to be their character, have them answer questions from the lender to see if they will get the loan.

Teacher Notes

The teacher notes page includes a paragraph with additional guidelines and things to think about as you begin to plan your lesson. This page also includes lines that you can use to add your own notes as you’re preparing for this lesson.

FINANCIAL LITERACY: BORROWING VS. SAVING TO BUY SOMETHING LESSON PLAN CONTENT PAGES

Saving

The Financial Literacy: Borrowing vs. Saving to Buy Something lesson plan includes three content pages. Sometimes, you want to buy something but don’t have enough money for it. To get enough money, you have two options: save it or borrow it.

Saving is when you put money aside for the future and don’t spend it right away. Different people have different strategies for saving money. Some people put a specific amount away each week or each month. Other people take a percentage of their money and set it aside. Many people put this money in a savings account at a bank.

It’s a great idea to create a savings plan if you want to buy something. For example, you might want to buy a new game console that costs $500 and you have a weekly allowance of $20. You decide to save half of your allowance ($10) each week until you have enough money to buy the game console. At that rate, it will take you almost a year to save up enough money! You can speed up the process by saving an addition $5 each week. However, it will still take you a long time to save enough money. Another possibility you might have is to borrow the money.

Borrowing

Borrowing is when you take something, like money, and use it temporarily. You can borrow clothes or a game from a friend, for example. Lenders are the people or institutions who you can borrow from. If you borrow something from a friend, you will need to return that item to them in the future. They might want to borrow something else from you in return!

When borrowing money from a person or bank, you need to pay them back with money at a later date. A friend might borrow $3 for ice cream. You can expect to get your $3 back later. This is different than when you give someone money to keep. When you borrow money from a bank, they always expect you to return the loan (the amount of money you borrowed from them) plus a fee called interest.

Loans and Credit

Loans are money that you borrow from somebody. They are often for a specific purpose or a sudden emergency. When you acquire a loan, you are acquiring debt. Debt is the money you owe. A lender, the person giving the money, will typically require that you pay back the loan plus interest. You calculate interest based on a percentage of the total amount you owe. The lender might also charge an addition fee. This is how banks make money!

Banks and credit unions typically give loans, but you might be able to also get a loan from a friend or family member. Financial institutions require a loan application, which asks for things like your income, your monthly expenses, your credit score, job history, and credit history.

Credit scores are three-digit numbers based on your credit and job history. The lender uses this number to determine whether or not they will give you a loan. If they approve you for a loan, they use your credit score to determine your interest rate. Your interest rate will typically be lower if you have a good credit score and work history. The higher the score, the better!

Lenders expect you to make a payment on your loan every month. Loan payments include both the principal, or the original amount you borrowed, plus interest. You will also make payments, sometimes called installments, over a specific period of time. We call this period of time the term of the loan. The formula that you can use to calculate how much interest you will pay on your loan is I = PRT (Interest = Principal x Rate x Time).

People borrow money by taking out loans all the time for different reasons. Some of these reasons could include paying for college, buying a house, buying a car, and starting a business.

Loans and Credit: Secured vs Unsecured Loans

There are two different kinds of consumer loans, secured loans and unsecured loans. With secured loans, the borrower has to back the loan with an asset, also called collateral, of near equal or greater value.

For instance, say your little brother needs $20 for a game and asks to borrow the money. You might be worried that you won’t get your money back, so you can require your little brother to give you an important baseball card, which is worth about $20. The baseball card is your collateral, and you get to keep the card if your little brother does not pay back his loan. You could then sell the card to make your money back or keep it and let it accrue value. You can even sell it back to him once he has enough money. Having collateral makes the loan less of a risk to you.

Banks do the same thing. When someone takes a loan out for a house or car, the bank might require collateral to make sure they’re able to get their money back.

With unsecured loans, on the other hand, there is no collateral needed to secure the loan. Student loans and personal loans do not have collateral requirements. Credit cards are one form of an unsecured loan. Even though they’re unsecured, you still always need to pay them back! If you repay your loan on time, the lender is more likely to lend you more (and sometimes larger amounts of) money in the future. Lenders won’t lend money to someone they don’t trust to pay them back.

Borrowing money can help you buy something that you need or want right away. However, this comes with the additional cost of interest. You’re paying more money to have something right now. Taking out loans is a great way to build your credit and improve your credit score. The better you are about making your payments on time, the better your credit score!

FINANCIAL LITERACY: BORROWING VS. SAVING TO BUY SOMETHING LESSON PLAN WORKSHEETS

The Financial Literacy: Borrowing vs. Saving to Buy Something lesson plan includes three worksheets: an activity worksheet, a practice worksheet, and a homework assignment. You can refer to the guide on the classroom procedure page to determine when to hand out each worksheet.

LOAN APPLICATION ACTIVITY WORKSHEET

For the activity worksheet, students will fill out a loan application, pretending that they make $2,000 a month.

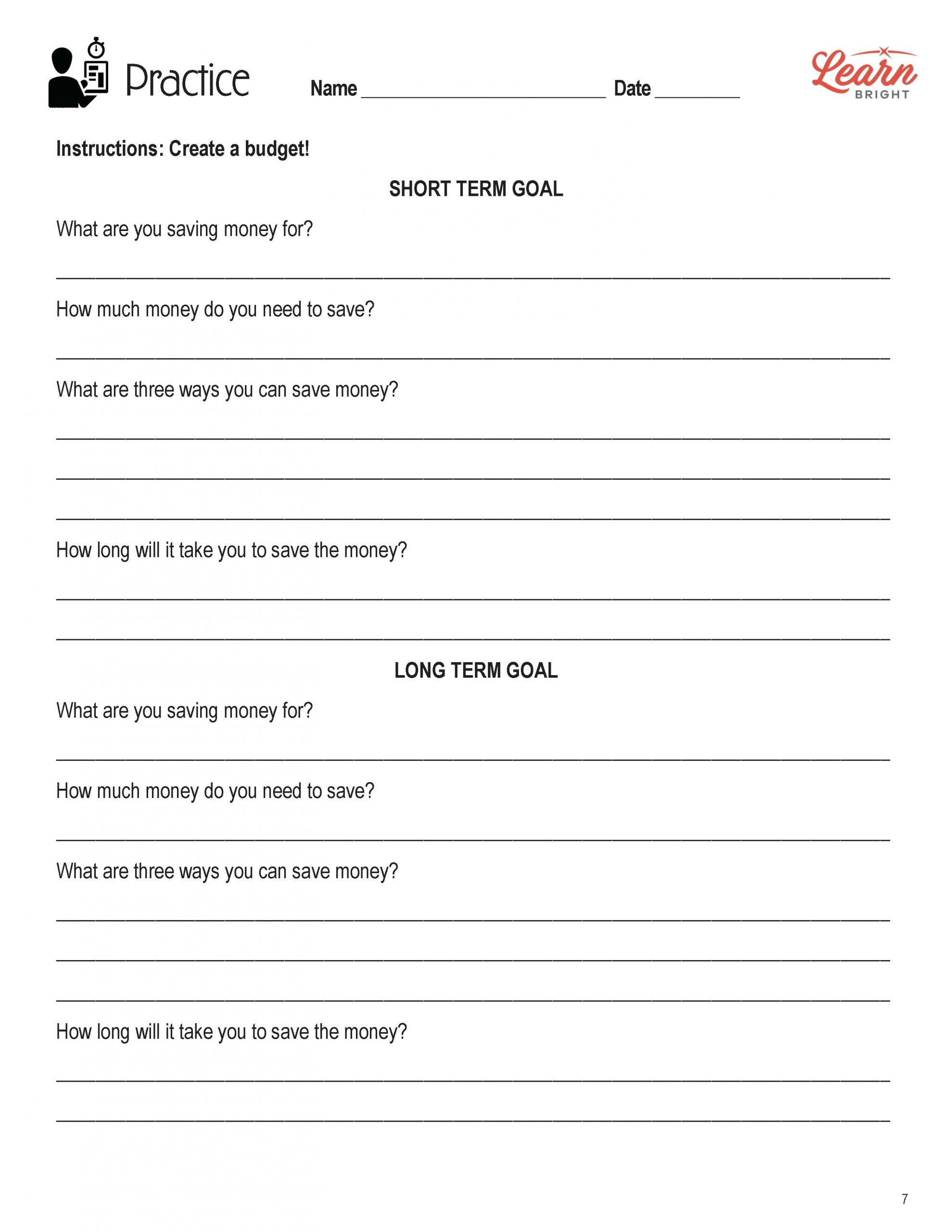

SHORT AND LONG TERM GOALS PRACTICE WORKSHEET

The practice worksheet asks students to create budgets for both a short term savings goal and a long term savings goal. They will answer questions about what they’re saving for, how much they’ll need to save, how they can save money, and how long it will take them to save money.

FINANCIAL LITERACY: BORROWING VS. SAVING TO BUY SOMETHING HOMEWORK ASSIGNMENT

For the homework assignment, students will answer questions about the lesson material to demonstrate their understanding.

Worksheet Answer Keys

This lesson plan includes answer keys for the practice worksheet and the homework assignment. If you choose to administer the lesson pages to your students via PDF, you will need to save a new file that omits these pages. Otherwise, you can simply print out the applicable pages and keep these as reference for yourself when grading assignments.